The Death of Graduate School?

The Republican tax plan is an odious hand-out to large corporations and a big 🖕 to most citizens and small businesses. Until I read this summary of the House Bill, I generally thought people who called Republicans corporatist bootlickers were being unfair. But here we are.

Anyway, two of the House Bill’s provisions are raising concerns about the future of postgraduate education:

- Treating tuition assistance and waivers as taxable income; and,

- Repealing the deduction for student loan interest.

These are both regressive measures that will make it harder for Americans to compete in the global economy, likely reduce the supply of doctors and nurses, and generally deprive a meaningful number of individuals of the pursuit of happiness.

But I would submit that, elite professional degree programs excepted, universities themselves are to blame for the impending decline of graduate education. They are buckling under the weight of their own failures to adapt to market realities—namely, price signals.

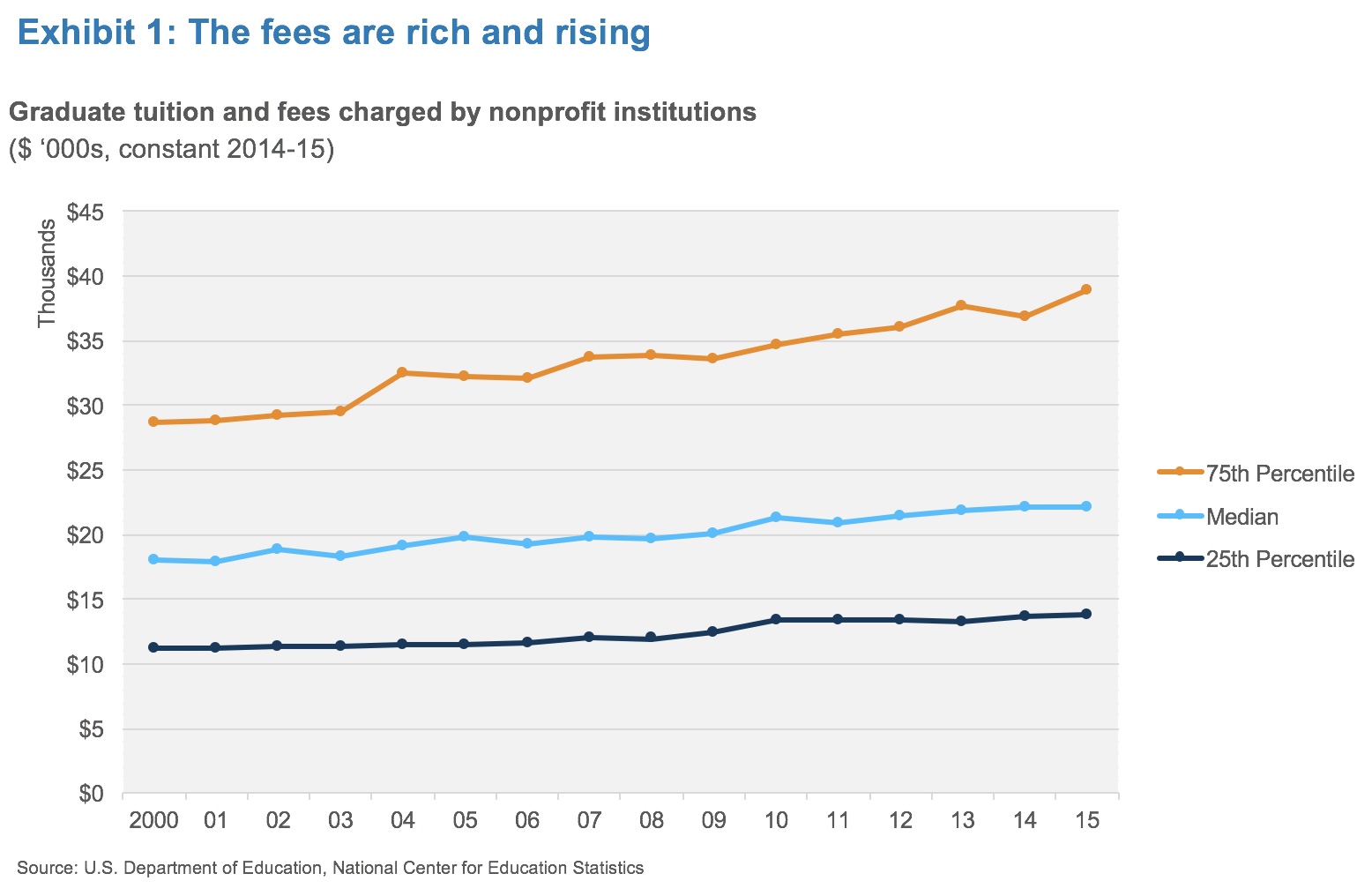

Graduate education is expensive

The median tuition and fees for graduate education at nonprofit U.S. institutions stood at $22,170 in 2015, implying an all-in cost of roughly $65,000 for a two-year master’s degree (assume two years of tuition, plus $10,000 / year in living expenses, books, etc.).1 This is the median, and it has grown 23% since 2000, in constant dollars.

The top-quartile breakpoint for tuition and fees clocked in at $39,000 in 2015, which would imply an all-in cost of $98,000 for a two-year master’s degree. Note that the fee spread between the top- and lower quartile breakpoints has expanded from roughly $17,500 in 2000 to $25,000 in 2015, a growth of 43% (see Exhibit 1). Again, constant dollars.

What is driving the increase in fees? There are several arguments on the supply side, but I will focus on the demand side.

Debt is the price of admission

Graduate education’s fees are beyond the means of most households. This is particularly true for those in the age brackets most likely to enroll: roughly 65% of grad students are 35 or younger.2 The median net worth for a U.S. household in 2013, excluding home equity, was $25,116.3 If you look at householders less than 35 years of age, the figure is $4,138. Moreover, 47% of the sub-35 age cohort have a net worth less than $5,000.

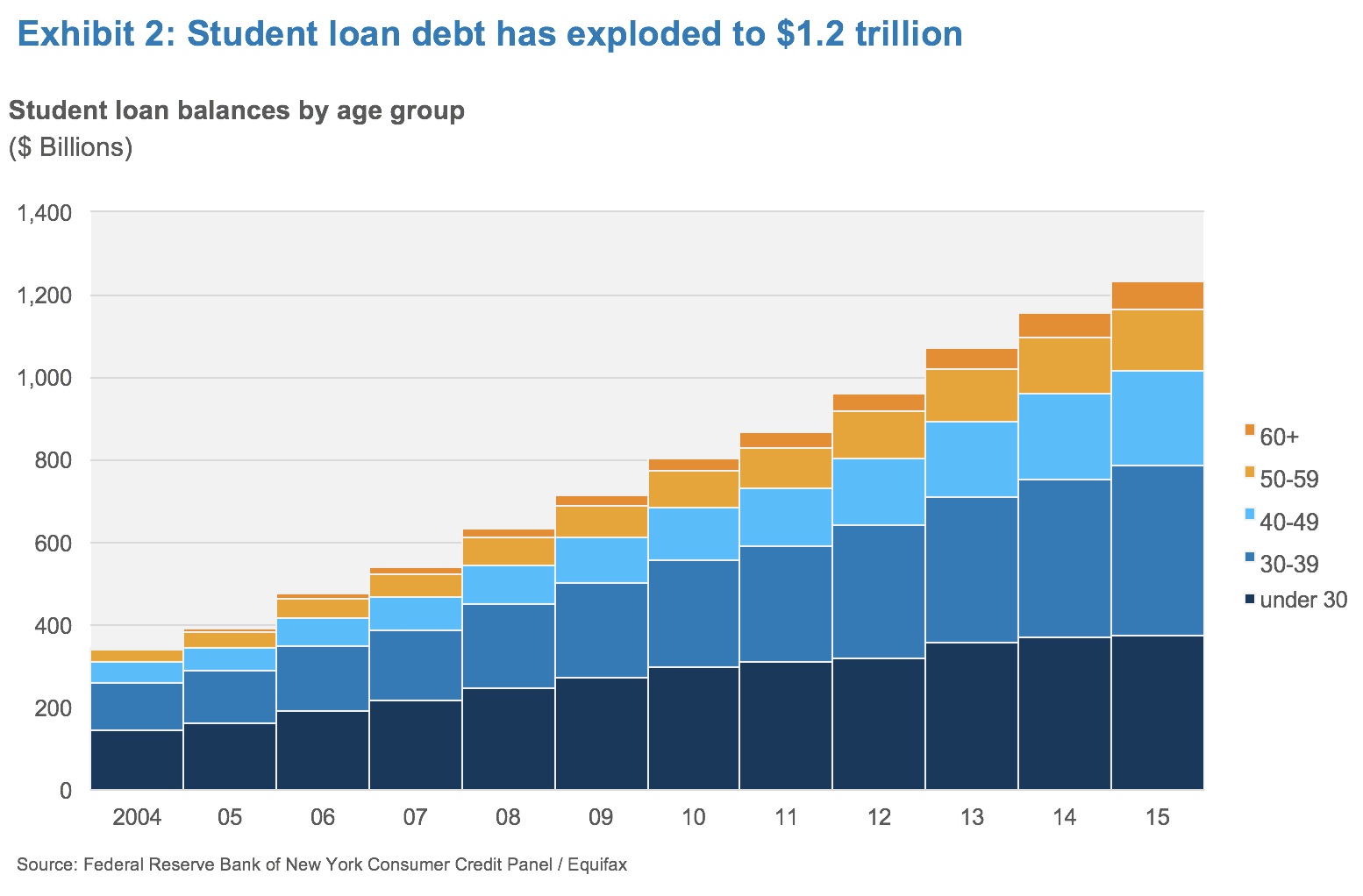

This blog has already covered U.S. households’ lack of savings and income growth; there’s no reason to believe that wages are keeping pace with the growth in tuition. Plainly, most students can’t pay out of pocket, so they must take on loans to cover the cost. Student loan balances have exploded from $350 million to $1.2 trillion over the last decade (see Exhibit 2), with analysis from the New America Foundation suggesting that graduate degrees are responsible for about 40% of the total.

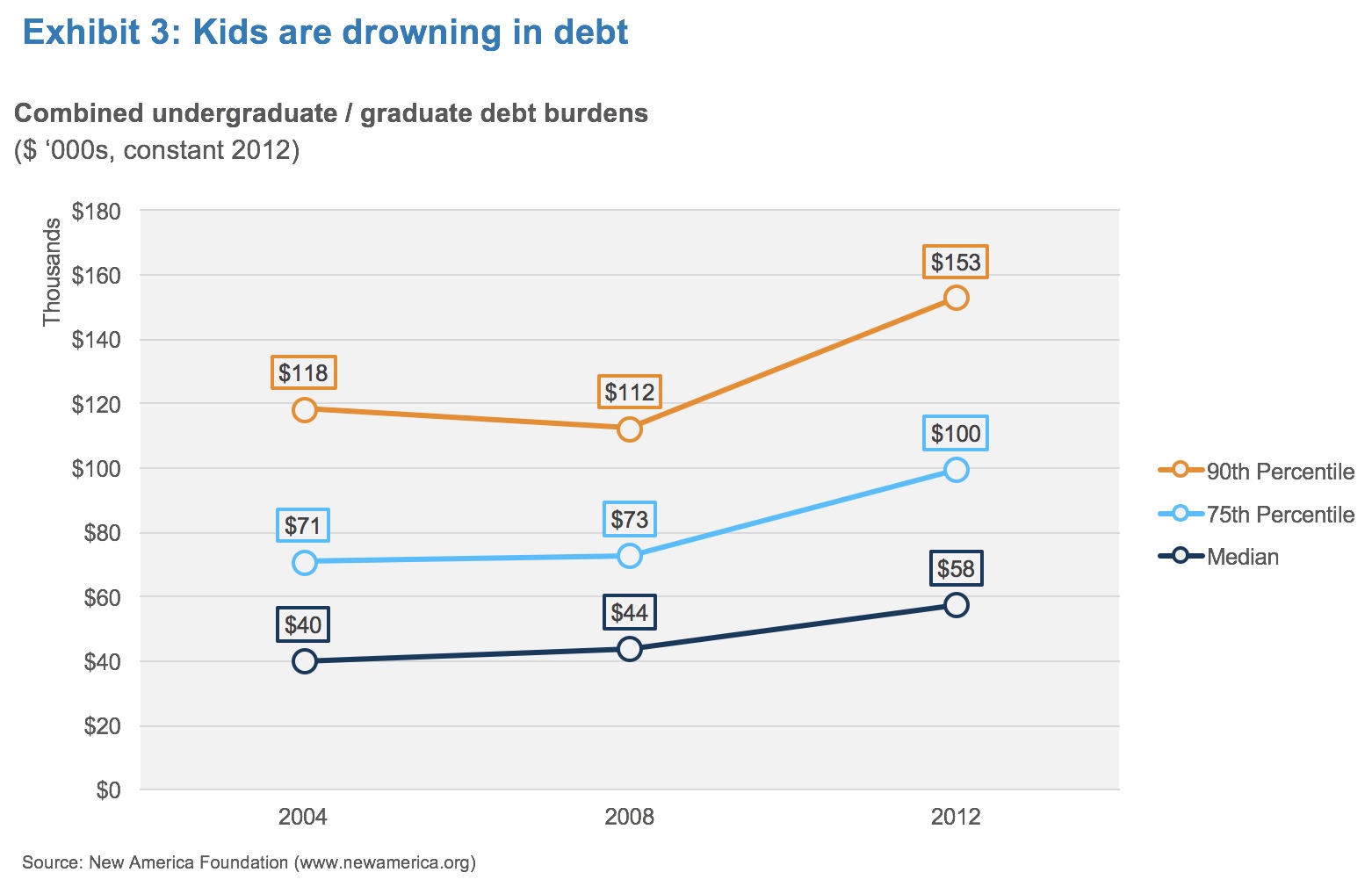

People are up to their eyeballs in graduate school debt. Figures from the New America Foundation show the median borrower owing nearly $58,000 in 2012, while 25% of borrowers owed $100,000 or more (see Exhibit 3).

Debt-financed graduate school is unsustainable

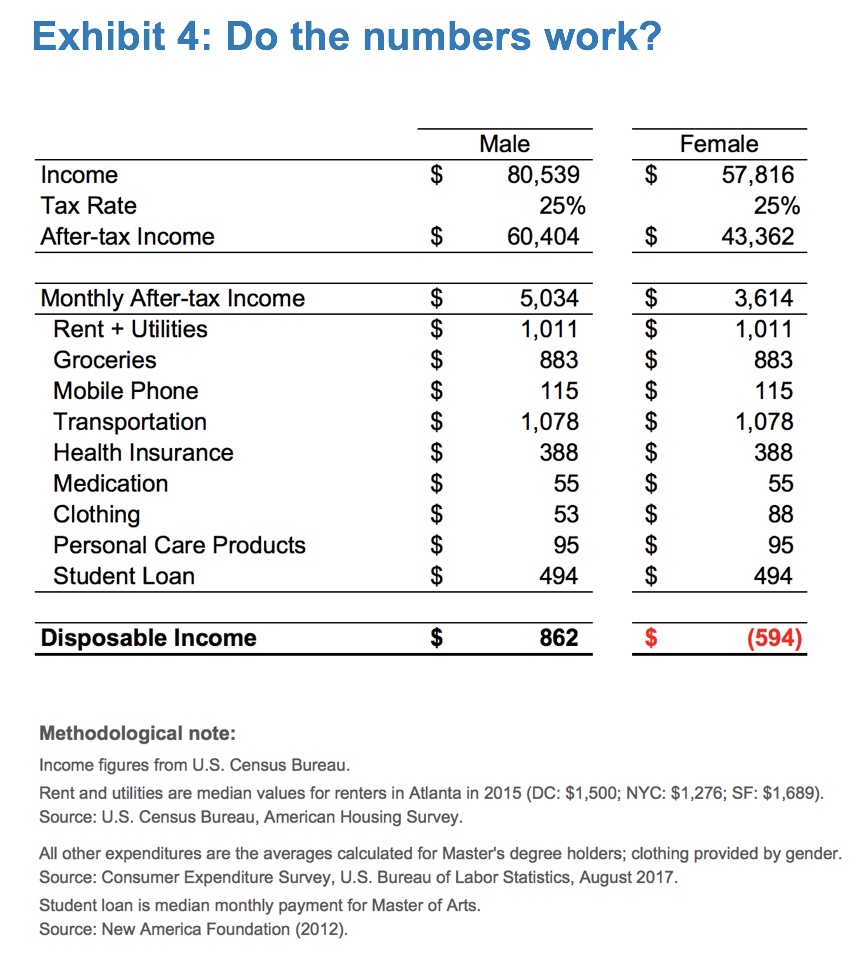

Consider the typical borrower. According to data from the U.S. Census Bureau, the median income for master’s degree holders in 2016 was $80,539 for males, and $57,816 for females. Let’s run a simple budget (see Exhibit 4).

Using somewhat reasonable assumptions on expenditures, the median male borrower has roughly $850 of disposable income per month, whereas the median female borrower can’t afford to live.

The gender gap is real and it must be closed. But leave that aside for a moment, and this exercise effectively demonstrates that a graduate degree is not worth pursuing for the median borrower unless her / his income is at least $75,000 after graduation.

But don’t stop there! Consider what’s not in this budget: savings (both near term and long term), medical expenses, day care. If our male borrower has a child, he can no longer afford to live.

The numbers don’t work. Demand is unsustainable at current price points.

The bonanza is over

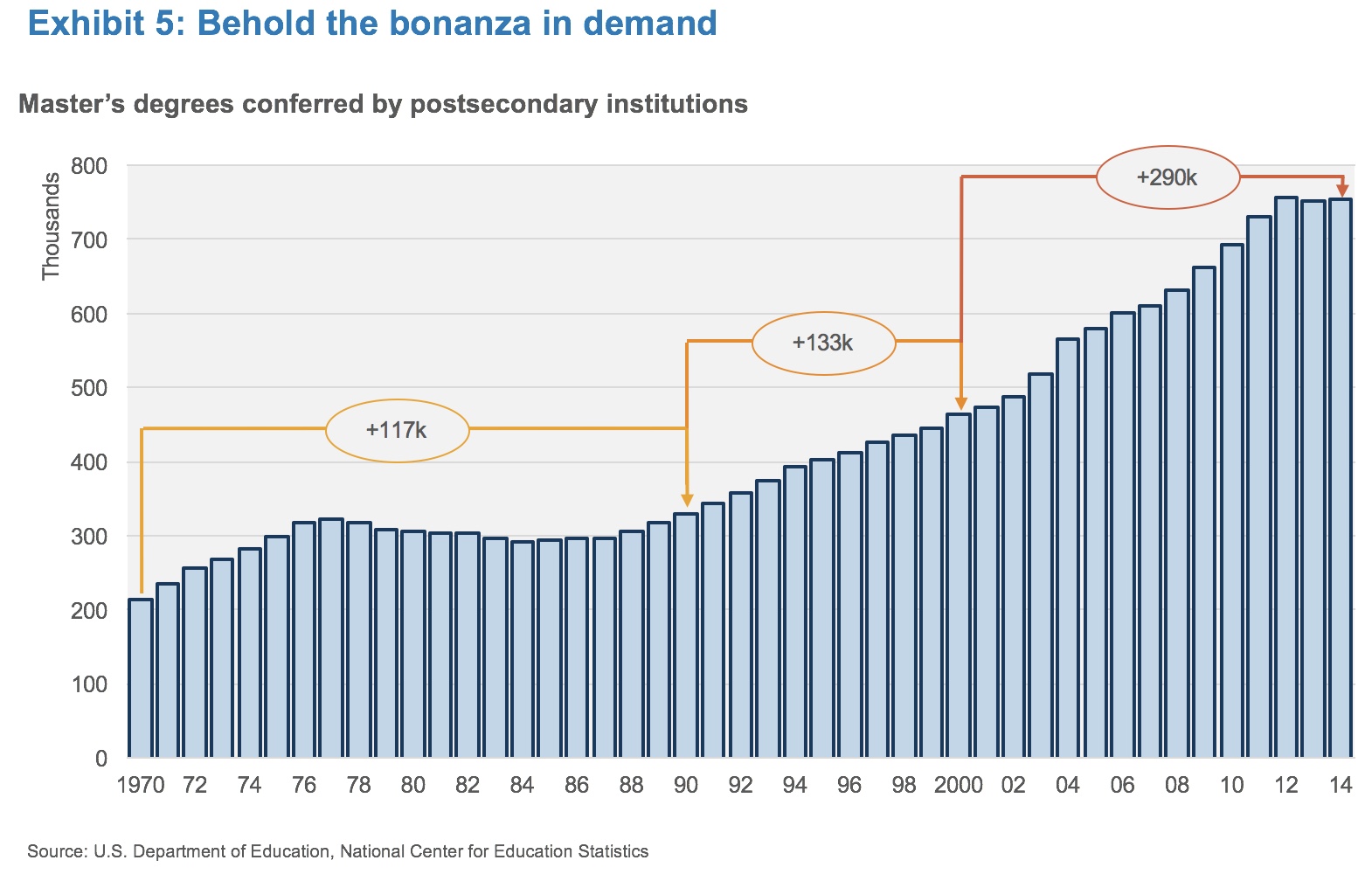

Graduate schools enjoyed a bonanza in enrollments over the last 15 years, with the total number of master’s degrees conferred rising from roughly 460,000 in 2000 to 755,000 in 2014 (see Exhibit 5). The step-up in growth is coterminous with the expansion in student loans beginning in 2004 (see Exhibit 2 above for a refresher).

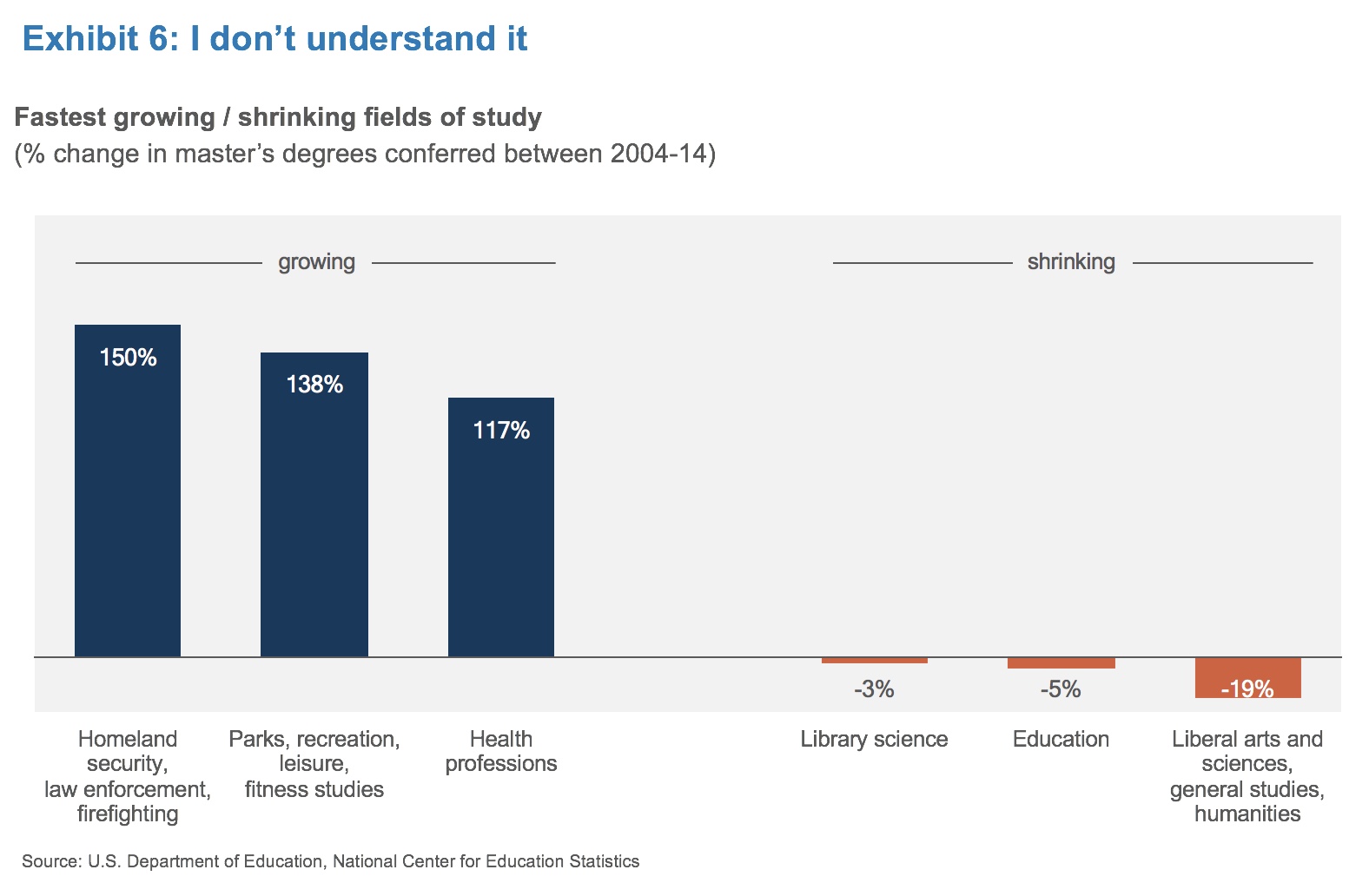

While business and education account for 45% of conferred master’s degrees, the fastest growing fields of study between 2004-14 were homeland security / law enforcement / firefighting, and parks / recreation / leisure / fitness studies (see Exhibit 6). Are master’s degrees necessary for these subjects? Is this credentialism gone mad? I digress …

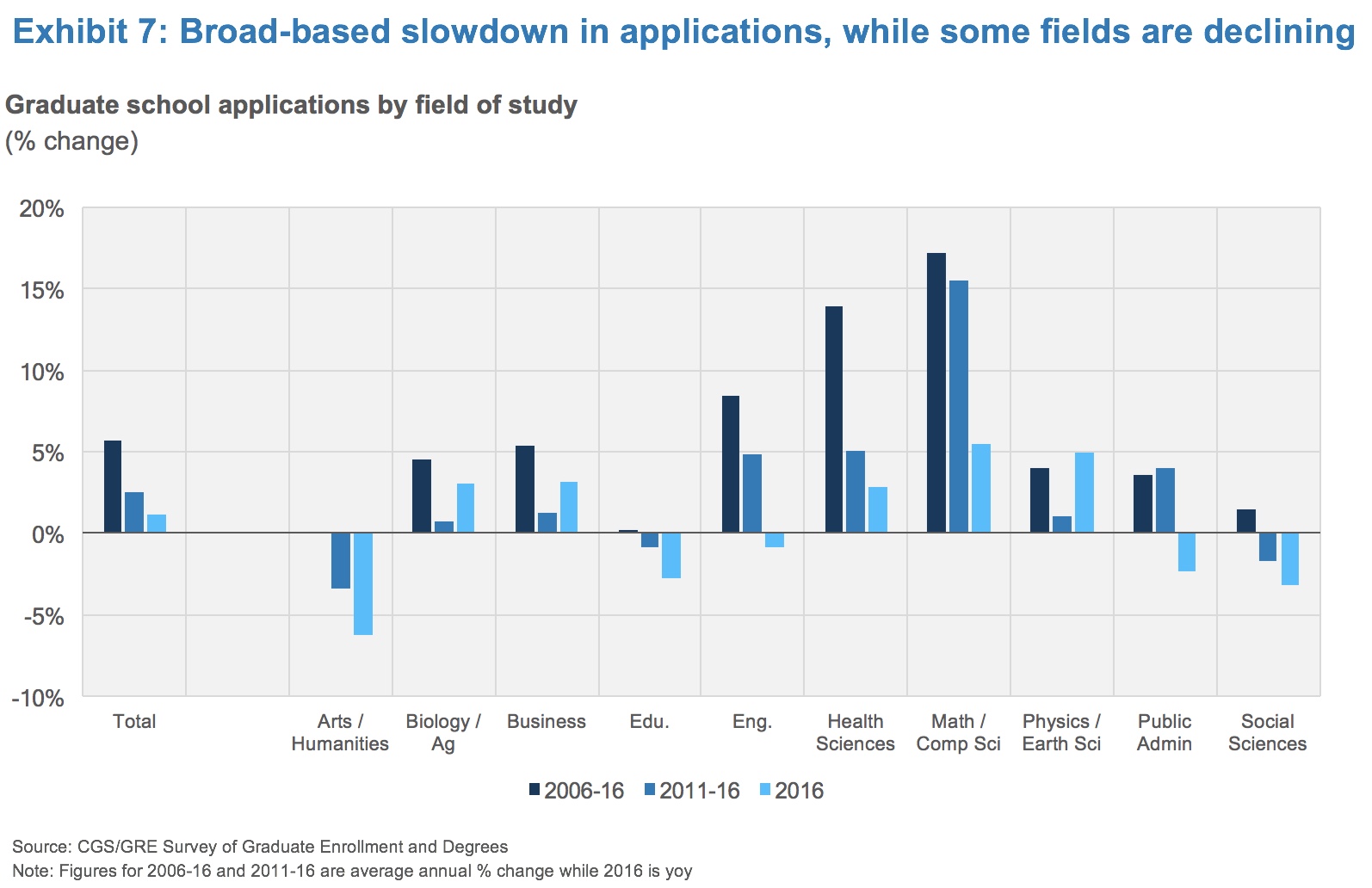

Anyway, this bonanza is coming to an end, as prospective students internalize the absolute and opportunity costs of graduate school, and scrutinize the value that postgrad degrees deliver. This is visible in the slowdown in applications for admission (see Exhibit 7).

Graduate school application growth rates have declined from an annual average of 5.7% in the decade to 2016, to 1.2% from 2015-16. The slowdown is visible across every field of study except physical and earth sciences. Notably, applications are actually declining in several fields, including arts and humanities, education, and the social sciences. Apparently David Rubenstein’s dictum that “humanities equals more cash” isn’t gaining traction.

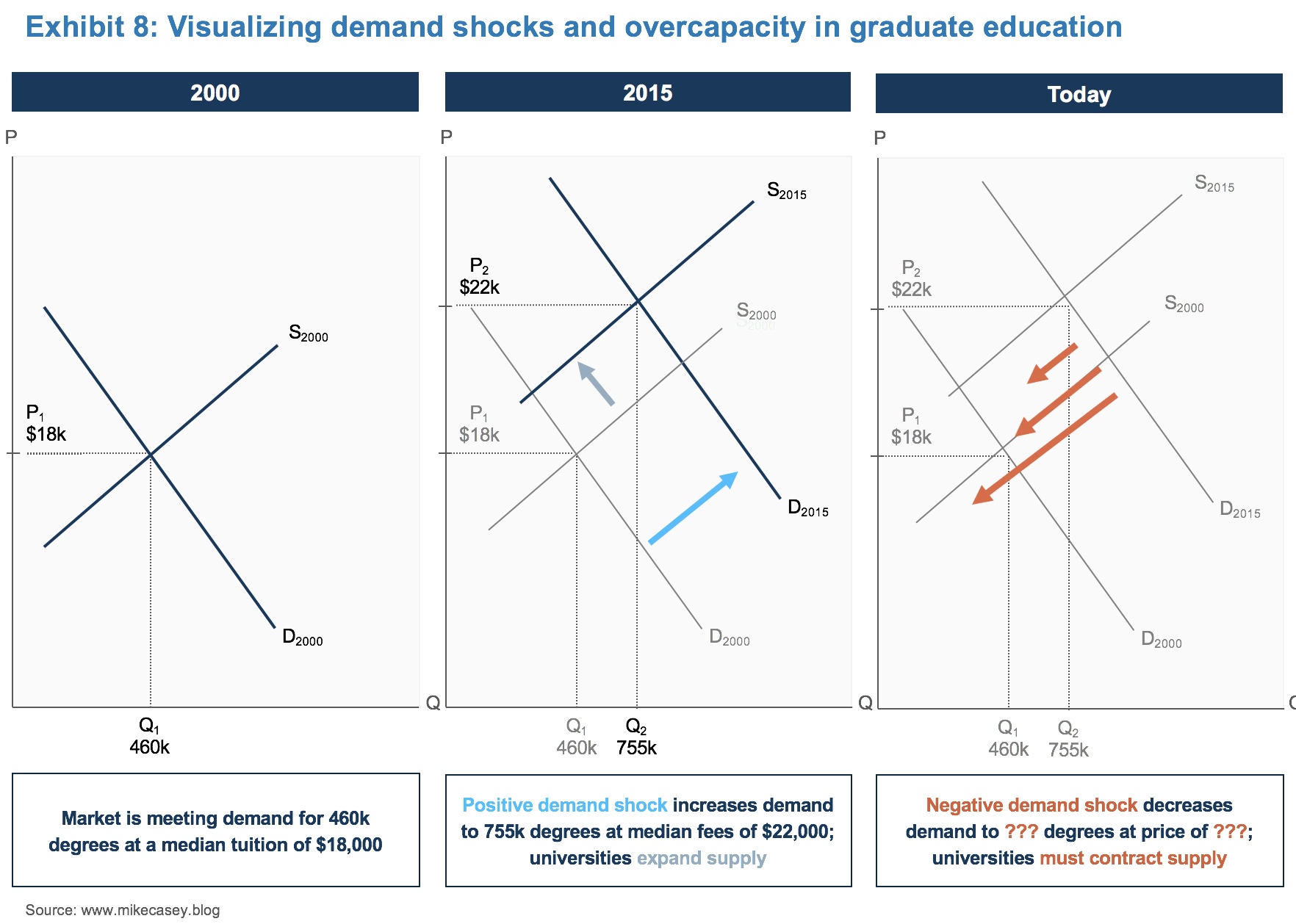

Now, consider what all these data points show (see Exhibit 8). In 2000, we can illustrate demand for 460,000 degrees at a median price of $18,000. In 2015, demand had increased by 64% to 755,000 degrees, while median prices increased by 23% to $22,000. Demand increased with prices! Graduate school is a Giffen good, only the “income effect” is driven not by changes in real incomes, but by access to debt with the expectation of future income gains.

The market experienced a demand shock. (I submit to you that it was driven by easier access to student loans, credentialism, and elite labor’s returns on graduate degrees.) Universities expanded their programming to meet demand at these higher prices. But now there’s an overcapacity of providers at inflated prices. The market now faces a negative demand shock.

The bottom line is that the graduate school business model is broken. It is predicated on the premise that graduate education increases students’ productivity and therefore wages, and that the universities can capture a chunk of this value. This is sound … up to a point. I suspect most programs’ pricing has passed this threshold. I believe the market has excess capacity for current domestic demand, and that international students now represent the marginal buyer.

Graduate education is dependent on the government-supported student loan market. The availability of subsidized and unsubsidized debt has enabled graduate programs to increase prices and therefore capture a larger share of students’ lifetime earnings. As a result, graduate schools effectively operate as an employment tax, and the government-supported loan market enables a wealth transfer from students’ futures to today’s academicians.

Elite institutions that produce elite labor will continue to justify their fees. Harvard Business School can charge what it wants, and most of its alumni will recoup the cost in a reasonable amount of time. But by definition, most institutions don’t produce elite labor. For many schools, the House Bill may reveal that demand for their product faces as precarious a future as the livelihoods of their customers. They must adapt to reality.

But let’s not leave Congress off the hook. Congress should move in the opposite direction. Rather than repealing the deduction on student loan interest, they should enable citizens to pay down student loans from pre-tax income. It is a good thing to incent people to save for retirement, health expenditures and even transportation costs through pre-tax plans. Why shouldn’t citizens be able to extract themselves more quickly from the yoke of student debt?

Footnotes

-

U.S. Department of Education, National Center for Education Statistics. ↩

-

Council of Graduate Schools, Data Sources: Non-Traditional Students in Graduate Education, available at https://cgsnet.org/ckfinder/userfiles/files/DataSources_2009_12.pdf. ↩

-

U.S. Census Bureau, Survey of Income and Program Participation, 2014 Panel, Wave 1 (Updated 13 November 2017). ↩