The American boy of 1854 stood nearer the year 1 than to the year 1900. The education he had received bore little relation to the education he needed. Speaking as an American of 1900, he had as yet no education at all. He knew not even where or how to begin.1

If science were to go on doubling or quadrupling its complexities every ten years, even mathematics would soon succumb. An average mind had succumbed already in 1850; it could no longer understand the problem in 1900 … At the rate of progress since 1800, every American who lived to the year 2000 would know how to control unlimited power. He would think in complexities unimaginable to an earlier mind. He would deal with problems altogether beyond the range of earlier society … The movement from unity into multiplicity, between 1200 and 1900, was unbroken in sequence, and rapid in acceleration. Prolonged one generation longer, it would require a new social mind. As though thought were common salt in indefinite solution it must enter a new phase subject to new laws. Thus far, since five or ten thousand years, the mind had successfully reacted, and nothing yet proved that it would fail to react—but it would need to jump.2

The Internet is the most deflationary invention of all time.3

A few weeks ago, the Fed determined that the world was not yet ready for a 25 basis point increase in U.S. interest rates. They’re smart and monetary policy is their day job, so I’m sure they know better than I about these things. But still, I find it all a bit befuddling.

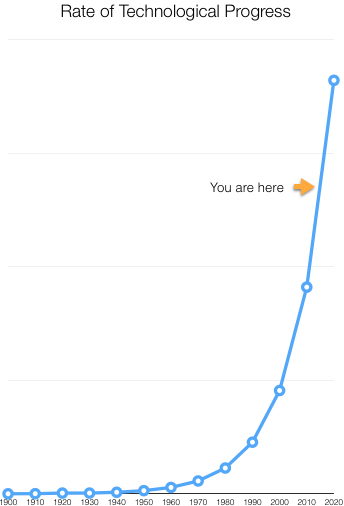

Lately I’ve been pondering whether monetary policy has been largely ineffective at generating inflation4 because the drivers of deflation aren’t monetary in nature, but rather technological. In 1904, Henry Adams developed a theory (“A Law of Acceleration”) on the exponential rate of technological change; and he posited that around the time we’re living in now, the rate of progress might exceed our ability to deal with it (see chart).

Just pause and reflect upon the most recent stories you’ve read / heard about:

- artificial intelligence

- batteries

- big data

- biomedicine

- energy

- information and communications technology

- miniaturization

- mobile

- particle physics

- processing power

- robotics

- satellites / GPS

- 3D printing

Technological advancements in these fields—and others—are driving down costs for many goods, services and labor, and they’re enabling remarkable innovation. Take a look at the list again and consider how many advancements were required to create the most recent iPhone. Then consider the number of industries in which the iPhone is helping to displace businesses. “Disruption” is destructive.

What’s particularly baffling is that while technology is contributing to deflation, the consumer surplus that technology is bringing about is massive and it is growing at a torrid pace. Consider the amount of free knowledge and entertainment available to someone with an iPad and an Internet connection—and how rapidly it has grown over the last decade. It’s not just the abundance of cheap products, it’s the ubiquity of free content and the erosion of pricing power.

I suspect this new era of consumer surplus is why Apple is crushing it. Apple creates the coolest products for accessing the most bountiful cornucopia of content in world history, and the company is exceptional at capturing value. It’s amazing.

In a world where so many can enjoy so much for so little, who will spend money and what will they spend it on? Absent a continuous expansion of household credit, how will technological progress impact personal consumption? Might we begin seeing a shift away from consumption-led growth in the U.S. economy (see chart)?

I have no idea.

Scott Galloway’s presentation on winners, losers and tech only left me with more questions:

Alas, it all makes me scratch my chin and wonder if the 20th Century paradigms about monetary policy no longer apply in this brave new world.

Think I’ll go read some Carl Hiaasen on a Kindle.

Further Reading:

The Reckoning | January 2014

The Squeeze Is On | February 2014

# # #

Notes:

1 Henry Adams, The Education of Henry Adams (Oxford World’s Classics: 2008), pg. 49.

2 Adams, op. cit., pgs. 413-4.

3 Todd Harrison, as quoted in Paul Vigna, “Minyanville’s Harrison: Online Media Model Is ‘Broken,’” Wall Street Journal, 20 May 2014.

4 Apart from in the notable exception of asset prices.

Comments

3 responses to “Technological Acceleration and the Wet Noodle of Monetary Policy”

You have plunged me into a rabbit hole of Andrew Keen and Jaron Lanier videos (all free on YouTube, of course). Need to read some of these books.

Great video!

Mike

The Galloway presentation was a good one — and I had a serious case of deja vu harking back to the late 1990’s, early 2000’s when we at PwC went all a-twitter (no pun intended) over the radical change that the internet/web might bring. What we overlooked in our enthusiasm were the systemic impacts. For that reason, I found another clip at the same conference featuring Andrew Keen — The Internet is Not the Answer — to be very relevant. Of course I immediately went to Amazon and downloaded into my Kindle (no gas stations converted to fulfillment points of presence here in Georgetown SC).